Flexible Deposit Mechanisms and Their Impact on Digital Number Draw Participation

Digital number draw platforms have expanded rapidly in recent years as payment technologies evolve and user expectations shift toward greater control over transaction timing and amounts. Deposit flexibility refers to the range of options available for funding accounts, including variable minimum thresholds, instant processing methods, scheduled transfers, and multiple payment channels such as e-wallets, bank transfers, and prepaid cards. Data from regulatory filings indicate that platforms offering tiered deposit structures see measurable differences in how often users log in and complete draws compared with those maintaining fixed high minimums.

Defining Deposit Flexibility in Number Draw Environments

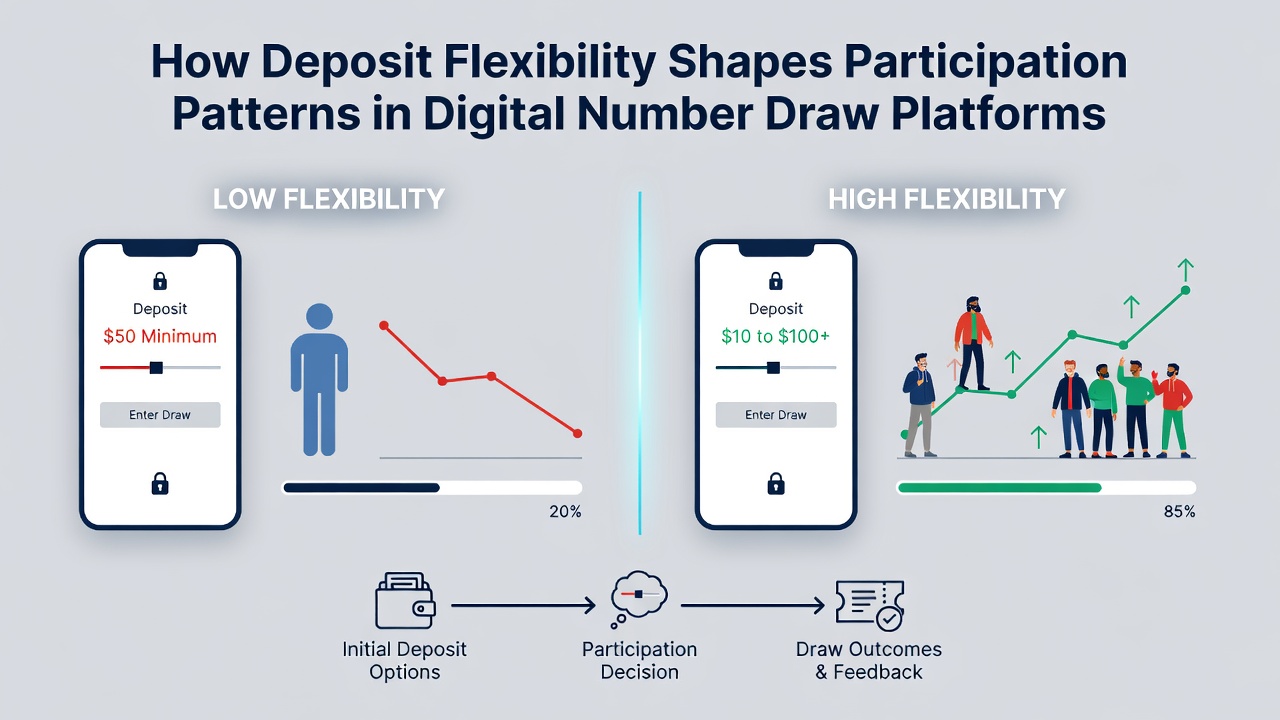

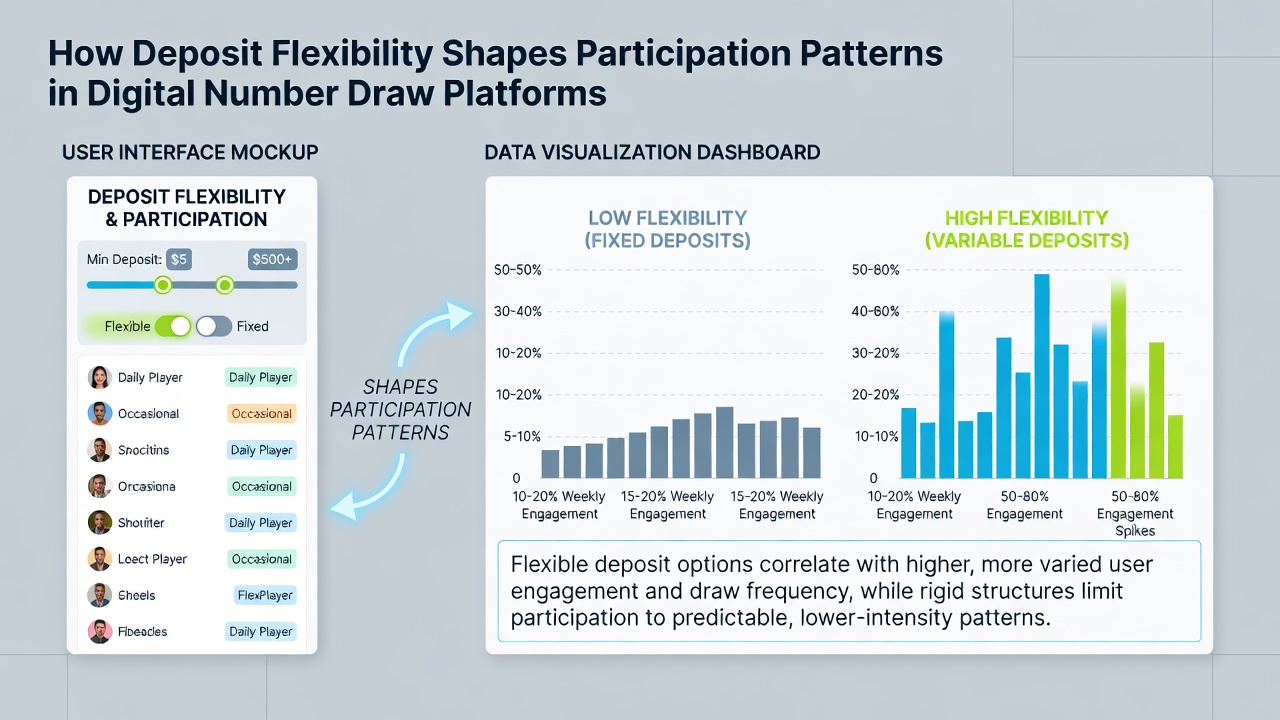

Operators structure deposit rules through several parameters that directly affect accessibility. Minimum deposit amounts range from fractions of a unit to larger fixed sums, while maximum limits and processing speeds vary by method. Research conducted by the Canadian Gaming Association shows that when platforms reduce entry barriers through lower minimums or instant-approval options, daily active user counts rise steadily across monitored periods. Payment protocols also incorporate features like recurring deposits and micro-transaction support, allowing participants to align funding with personal cash-flow cycles rather than platform-imposed schedules.

Those who have analyzed transaction logs note that deposit flexibility correlates with session length and frequency. Platforms permitting deposits as low as one unit record higher repeat engagement rates, whereas rigid structures concentrate activity among fewer high-value accounts. Observers point out that this pattern holds across different regulatory jurisdictions because the underlying mechanics remain consistent regardless of geographic location.

Participation Patterns Linked to Deposit Structures

Participation data reveals distinct clusters when deposit options diversify. One pattern involves sporadic users who engage only when convenient funding methods align with their schedules, producing irregular but sustained activity spikes. Another cluster consists of regular participants who utilize scheduled deposits to maintain consistent draw entries, resulting in steadier revenue streams for operators. Figures released by the New Jersey Division of Gaming Enforcement in early 2026 demonstrate that platforms introducing flexible deposit tiers experienced a 17 percent increase in unique participant accounts over a six-month window ending in May.

Demographic breakdowns further illustrate these effects. Younger cohorts tend to favor instant e-wallet deposits with minimal thresholds, leading to shorter but more frequent sessions. Older groups often select bank-linked recurring transfers, which support longer commitment periods but fewer daily interactions. Analysts tracking these trends through June 2026 report that hybrid models combining both approaches capture broader population segments without requiring separate marketing campaigns for each group.

Regional Regulatory Influences on Deposit Options

Regulatory frameworks shape the boundaries within which operators can experiment with deposit flexibility. In Ontario, the Alcohol and Gaming Commission permits variable minimums provided consumer protection thresholds remain intact, resulting in platforms that test multiple tiers simultaneously. Australian state regulators have similarly authorized instant processing for verified accounts while requiring clear disclosure of fees, producing participation data that shows elevated engagement in jurisdictions with streamlined deposit pathways.

European markets present additional variation because national rules differ on transaction speed and verification requirements. Platforms operating across borders often maintain separate deposit configurations for each region, and internal reports indicate that localized flexibility increases cross-border user retention when compared with uniform global settings. Data compiled through mid-2026 confirms these adjustments produce measurable shifts in draw completion rates without altering prize structures or game rules.

Operational Adjustments and User Response Metrics

Operators respond to observed patterns by refining deposit interfaces in real time. When transaction data indicate drop-off at certain minimum thresholds, many adjust those levels downward and monitor subsequent log-in frequency. One documented case involved a platform that lowered its baseline deposit from five units to one unit; within eight weeks, the number of weekly active accounts grew by 22 percent according to internal analytics shared with industry partners.

Payment method diversity also plays a measurable role. Platforms supporting four or more distinct channels record lower abandonment rates during funding steps than those limited to two options. Researchers examining aggregated logs across multiple sites note that users encountering failed transactions on a single method often abandon the session entirely unless alternative channels appear immediately. This dynamic underscores why many operators now present deposit choices in a single consolidated screen rather than sequential menus.

Conclusion

Deposit flexibility continues to function as a primary variable shaping participation across digital number draw platforms. Evidence from regulatory reports and transaction analyses demonstrates consistent relationships between minimum thresholds, processing speeds, and user engagement metrics. As platforms refine these parameters through 2026, participation patterns evolve in predictable directions tied directly to the range of funding options each system provides.